By Betweenplays Media Albert Laurin – Investigative Feature

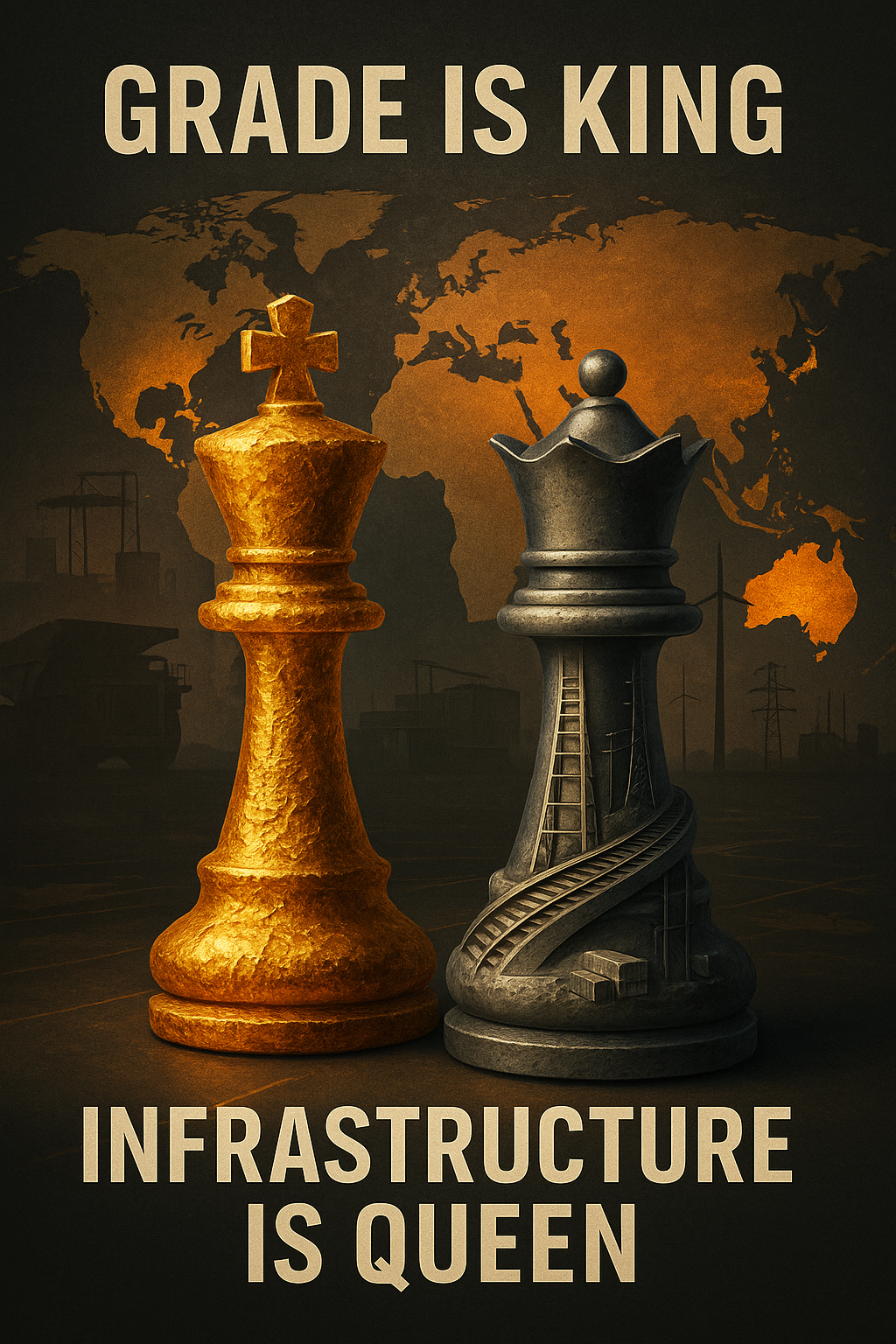

Grade Is King, Infrastructure Is Queen: Mining’s Global Playbook from Australia’s Dominance to the Americas’ Potential

By Betweenplays Media – Investigative Feature

Introduction

Mining underpins the 21st century. From the copper in transmission lines to the lithium in EV batteries and the cobalt stabilizing cathodes, mined resources are the foundation of our infrastructure, technology, and energy systems.

Yet, as demand surges, the industry faces intensifying complexity: geopolitics, ESG pressures, financing discipline, technological shifts, and public skepticism. To succeed, mining projects must now pass a far tougher test — one captured by a phrase repeated in boardrooms and analyst calls alike: “Grade is King, Infrastructure is Queen.”

This article explores what that really means in practice. It dives into how projects are assessed by investors, CEOs, bankers, and global asset managers; how jurisdictions like Australia have become dominant players; the roles of giants like Ganfeng and CATL; and which companies in the Americas might one day match them.

It also highlights a Betweenplays exclusive — an in-depth conversation with Brunswick Exploration CEO Killian Charles, who took off his CEO hat to speak candidly like the analyst he once was.

1. The Immutable Truth — Grade and Infrastructure

Grade refers to the concentration of the target mineral in the ore. In gold, it’s measured in grams per tonne (g/t); in copper or nickel, as a percentage. Higher grade means more payable metal per tonne of material mined, lowering costs and protecting margins when prices fall.

Infrastructure covers the logistics and utilities that make a mine viable: roads, rail, ports, grid power, water supply, and increasingly — access to refining or chemical processing capacity.

Without grade, economics falter. Without infrastructure, grade stays in the ground.

Consider the Greenbushes mine in Western Australia — the world’s largest hard-rock lithium operation, producing about a third of global spodumene supply. Its success isn’t just geology; it’s proximity to processing plants, ports, and skilled labor.

2. The Harsh Reality of Timelines

Bringing a mine into production is slow. According to S&P Global Market Intelligence, the average lead time from discovery to production is 15.7 years globally. For projects discovered between 2010–2019, that stretches to nearly 18 years.

The U.S. fares even worse, averaging 29 years, largely due to permitting complexity, multi-agency reviews, and litigation.

Even in mining-friendly jurisdictions, delays often stem from infrastructure buildouts. A road, rail spur, or transmission line may require its own environmental assessment and multi-year approval process.

MESSAGE TO READER: On August 9th, 2024, a catastrophic backflow flood — triggered by extreme weather — inundated my home and studio with over 3½ feet of contaminated water. The disaster destroyed all broadcasting equipment, wiped out my HVAC system, and forced a full-scale demolition and sterilization of the basement. The rebuild required months of intense, hands-on labor, further complicated by a serious inguinal hernia caused by the physical strain of recovery work, which later required surgery.

Despite the loss of a year of production for Betweenplays Media, the crisis became a period of behind-the-scenes rebuilding — upgrading the studio, mastering new editing skills, expanding professional networks, and re-strategizing content direction.

Now, in September 2025, the payoff is here: interview requests are piling up, high-profile opportunities are lining up back-to-back, and the platform is entering a sustained growth phase. What began as a nightmare has become the foundation for the strongest relaunch in the brand’s history.

3. Concentration, Chokepoints, and Geopolitical Leverage

Mining is global, but processing is hyper-concentrated. The International Energy Agency reports that China processes 19 of 20 critical minerals, including over 80% of rare earths and battery-grade graphite.

This has fueled strategic responses:

- Indonesia banned nickel ore exports, forcing in-country processing (Reuters).

- Chile is consolidating lithium under state-led partnerships, with Codelco taking a lead role.

- The EU Critical Raw Materials Act mandates by 2030 that 10% of strategic raw materials be mined domestically, 40% processed in the EU, and 25% recycled (EU CRMA text).

4. The Investor’s Playbook

Professional investors screen mining projects through several lenses:

- Grade & Recovery — Can the project stay profitable if prices drop 30%?

- Infrastructure — Distance to roads, rail, port, power, and water; haulage cost per tonne-km.

- Jurisdiction Stability — Rule of law, taxation, and community relations.

- Processing Access — Is there a smelter, refinery, or conversion plant nearby?

- Timeline Position — Is it still in exploration, or permitted and shovel-ready?

- Capital Stack — Debt, equity, streaming/royalty burden.

- Policy Exposure — Is it at risk from export bans or nationalization?

A project with high grade, strong infrastructure, a mining-friendly jurisdiction, and a clear financing/offtake plan is often a takeover target.

5. The CEO’s Lens — Orchestrating Complexity

From the operator’s side, the job is part engineering, part diplomacy:

- Roads, Rail, Ports — Who funds construction? Are roads built for haul truck weights? Are ports ice-free year-round?

- Power — Is there nearby hydro or grid tie-in? How costly is a substation build?

- Water — Reliable year-round source, treatment requirements, discharge compliance.

- Tailings — Global Industry Standard on Tailings Management (GISTM) compliance is now a baseline.

- Community/Indigenous Partnerships — In Canada, the Supreme Court’s Haida ruling makes consultation a legal requirement.

- Midstream Access — Without refining/conversion capacity, raw product risks bottlenecks or low netbacks.

Execution is an all-fronts campaign against time, capital burn, and public scrutiny.

6. Banks, Capital Markets, and Financing Discipline

Financiers aren’t swayed by geology alone. To unlock debt and equity:

- NI 43-101 / JORC-compliant Feasibility — Conservative price decks, third-party verification.

- Credible Offtakes — With prepayment and floor-price protections.

- Balanced Streaming/Royalties — Avoiding NPV erosion.

- ESG Governance — OECD due diligence on human rights and environment.

- Realistic Timelines — Permitting and construction schedules that reflect jurisdictional realities.

7. Tier-One Asset Managers — Strategy with Sources

BlackRock

- Identifies the low-carbon transition as one of its “mega forces” driving capital reallocation (BlackRock).

- Launched a “brown-to-green” materials fund in 2025 to back miners with credible decarbonization plans (ESG Dive).

- Energy & Resources Income Trust has shifted toward transition-aligned commodities.

JPMorgan

- Forecasts copper at ~$8,300/t in Q2 2025, noting potential downside from tariffs (JPMorgan).

- Stresses that near-term caution coexists with long-term electrification demand.

Vanguard

- Uses its stewardship clout to push for tailings safety, climate risk disclosure, and governance.

8. Canada — Infrastructure Edge, Legal Reality

Canada has world-class advantages:

- Low-carbon hydro (Hydro-Québec).

- Rail & Ports — Vancouver, Prince Rupert, Sept-Îles, Halifax.

But the constitutional duty to consult Indigenous peoples can lengthen timelines, as seen in Ontario’s Ring of Fire.

9. Ethics — The Cobalt Dilemma

Amnesty International and others have documented child labor in DRC artisanal cobalt. Shareholder pressure led Tesla to commit to reducing cobalt use after Battery Day 2020.

Hypocrisy is real: rejecting local mines while importing ethically questionable metals. The fix is building domestic/allied supply with transparent ESG compliance.

10. Betweenplays Exclusive — When a CEO Thinks Like an Analyst

In a standout interview, Brunswick Exploration CEO Killian Charles drew on his analyst background to explain what professionals truly look for:

- Grade & scale

- Infrastructure proximity

- Jurisdiction stability

- Management execution capability

- Financing and offtake certainty

This wasn’t theory — it was the applied mental framework institutional players use.

“Exclusive: CEO Killian Charles Reveals the Analyst Mindset Driving Market Decisions”

11. Why Australia Wins — and Americas’ Aspirants

Australia’s Playbook

- Top producer of lithium, iron ore, bauxite; top 5 in gold, nickel, uranium.

- Mining is 15% of GDP and 75% of exports (minerals.org.au).

- Infrastructure-first policy: integrated rail, ports, and energy.

- Government investment in refining — e.g., Iluka rare-earth refinery.

Ganfeng & CATL

- Ganfeng Lithium — vertically integrated, global lithium leader.

- CATL — world’s largest EV battery producer, securing upstream mineral supply.

Americas Contenders

- Lithium Americas (Argentina/USA) — Thacker Pass and Cauchari-Olaroz projects.

- SQM (Chile) — lithium giant with global reach.

- First Quantum (copper) and Sigma Lithium (Brazil) — growing influence.

12. The Cheat Sheet

Investor: Grade + infrastructure + jurisdiction + finance = value.

Operator: Roads, power, water, tailings, partnerships — execution follows.

Banker: Feasibility, ESG compliance, realistic timelines.

Geopolitics: Control processing, not just mining.

Ethics: Domestic/allied supply with OECD-grade transparency.

Global Lesson: Australia’s infrastructure, scale, and policy are unmatched; Americas must accelerate timelines and local processing to compete.

Alright — here’s a powerful conclusion that leaves the reader with both strategic insight and urgency, followed by a professional disclaimer that protects you legally, and then I’ll give you an image concept that’s visually worthy of the article.

Conclusion — Mining’s Next Decade Will Crown New Kings and Queens

The mining industry of the next decade will not be won by those who simply find ore. It will be won by those who marry geology to infrastructure, align capital with credibility, and uphold ethics as fiercely as efficiency.

The new kings will be the companies that can drill high-grade deposits, build or access roads and ports, lock in power and water, and deliver product to market through secure refining channels. The new queens will be the infrastructure networks — physical and political — that allow those resources to flow without interruption.

Australia has proven this model works. The Americas are rich in resources but lag in speed, infrastructure, and processing capacity. Closing that gap will require political will, cross-border cooperation, and capital discipline on a level the region has not yet seen.

The paradox remains: nations and investors that reject mining in their own backyards but fund it abroad in jurisdictions with weaker safeguards are building fragile supply chains and moral contradictions. The path forward is clear — build at home, build responsibly, and build to last.

In mining, the cycles are inevitable. But those who get the fundamentals right — grade, infrastructure, governance, and market access — will not just survive them. They will define the next era.

Disclaimer

The information presented in this article is provided for informational and educational purposes only. It does not constitute investment advice, financial guidance, or a recommendation to buy or sell any security, commodity, or other financial instrument. The views expressed are based on publicly available information, industry research, and interviews, and while believed to be accurate at the time of writing, no guarantee is made as to their completeness or correctness.

Readers and viewers are encouraged to conduct their own due diligence, consult with licensed financial advisors, and consider their individual risk tolerance before making any investment decisions. Betweenplays Media and the author assume no liability for any actions taken based on the content of this article.

Coming Soon; A novel by Betweenplays Media “Global Fracture“

TAGS: only commas, no hashtags, #GlobalFracture, #StockMarketNews, #InvestorMindset, #MacroTrends, #FinancialLiteracy, #MarketWatch, #Geopolitics, #EconomicShift, #TradeWars, #ResourceRivalries, #BRICSvsNATO, #InvestSmart, #InvestmentOpportunities, #FinanceNews, #CapitalMarkets, #EquityMarkets, #CommodityMarkets, #Betweenplays, #Viewertainment, #Over40000Subscribers, #InvestorCommunity, #WallStreet, #TSX, #NYSE, #MarketUpdates, #FinancialInsights, #WestIslandRealEstate, #MontrealRealEstate, #WestIslandBroker, #MontrealBroker, #PointeClaireHomes, #DollardDesOrmeaux, #KirklandRealEstate, #BeaconsfieldHomes, #DDORealEstate, #MontrealWestIsland, #LuxuryRealEstateMontreal, #MontrealHomeForSale, #BuyAHomeMontreal, #SellYourHomeMontreal, #CourtierImmobilier, #CourtierWestIsland, #MontrealEnglishCommunity, #GreaterMontrealRealEstate, #LaurinImmobilier, #WestIslandHomes, #MontrealCondos, #MontrealPropertyMarket, #BuySellInvestMontreal