By Betweenplays Media 🎙️ — August 2025

Abstract

The global transition toward electrified transportation is now defined by a high-stakes contest among battery manufacturers, whose technologies and production capabilities determine the pace, cost, and scale of electric vehicle (EV) adoption. This thesis examines the current leaders in EV battery production — companies already supplying batteries for EVs in mass production or poised to do so imminently — with a focus on their technological strategies, geographic reach, and market impact. The analysis reveals a landscape dominated by Chinese, South Korean, and Japanese manufacturers, with emerging players in Europe and the U.S. preparing to challenge incumbents through next-generation battery chemistries, regional production hubs, and strategic OEM partnerships.

Introduction

Electric vehicles have transitioned from niche products to core elements of national transportation strategies. Central to this shift is the EV battery — the single most expensive and technologically complex component of an electric vehicle. Battery performance defines an EV’s range, cost, charging time, and safety profile, while battery production capacity dictates the global supply chain’s ability to meet surging demand.

As of 2025, the EV battery industry is entering a decisive phase:

- Global EV sales are projected to surpass 18 million units in 2025, representing over 20% of new vehicle sales worldwide.

- Battery manufacturing capacity is consolidating around a handful of large-scale producers with advanced cell chemistry and vertically integrated supply chains.

- Next-generation battery technologies — including semi-solid-state and solid-state chemistries — are beginning to reach commercial deployment.

This paper identifies the top companies actively delivering EV batteries into vehicles on the road today or in the immediate future, analyzes their technological strategies, and evaluates their impact on the evolving EV ecosystem.

The Competitive Landscape of EV Battery Manufacturing

Market Concentration and Geographic Dominance

The EV battery market remains highly concentrated, with the top five producers accounting for over 80% of global supply.

China dominates both production volume and supply chain control, followed by South Korea and Japan, with Western manufacturers currently dependent on joint ventures or licensing arrangements to scale production.

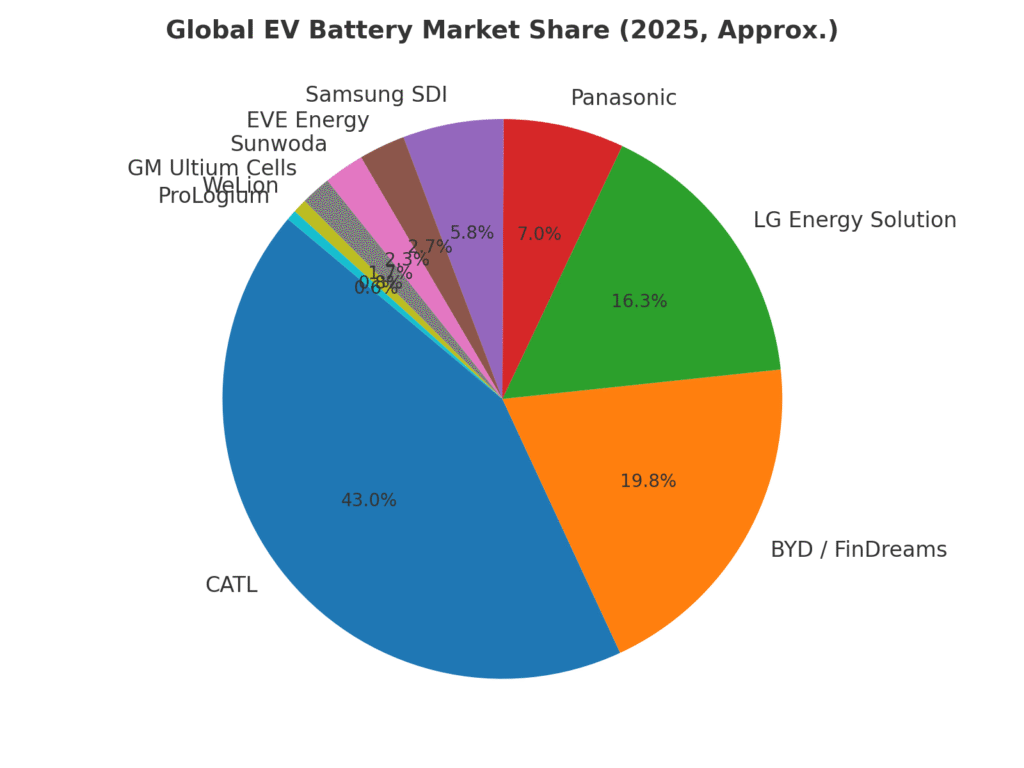

Figure 1 — Global EV Battery Market Share (2025, Approx.):

Company Profiles and Technology Strategies

1. CATL (Contemporary Amperex Technology Co.)

- Global Market Share: ~37% — the largest EV battery supplier worldwide.

- Key Chemistries: LFP (Lithium Iron Phosphate), NCM (Nickel Cobalt Manganese), LMFP (Lithium Manganese Iron Phosphate), and sodium-ion.

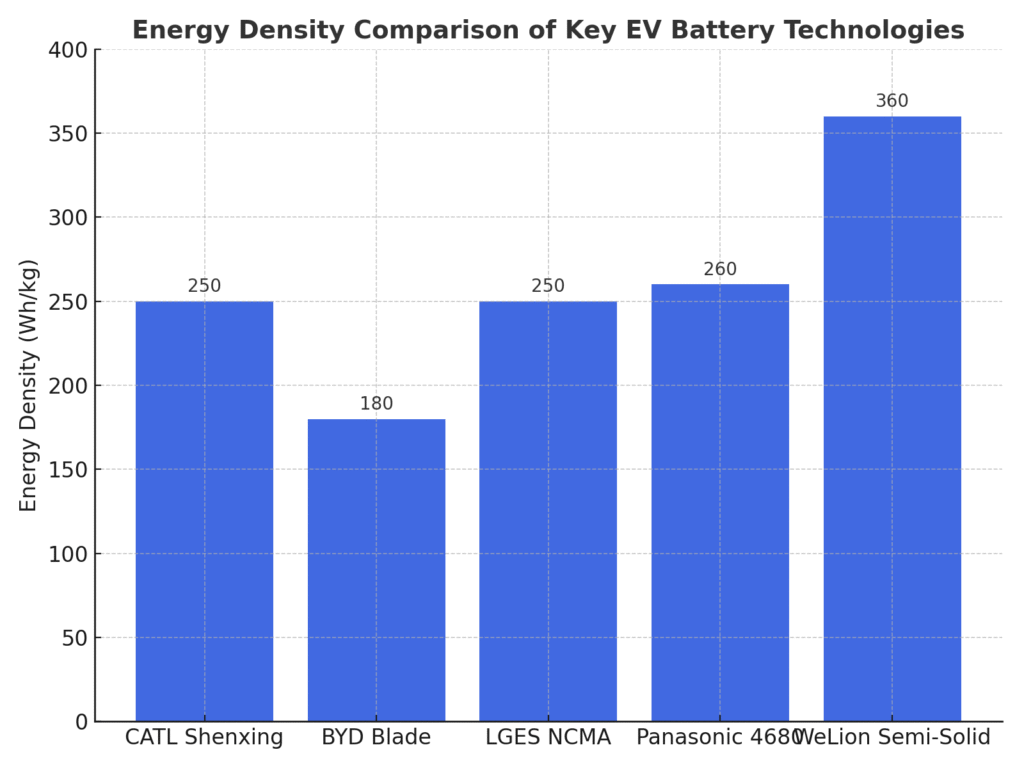

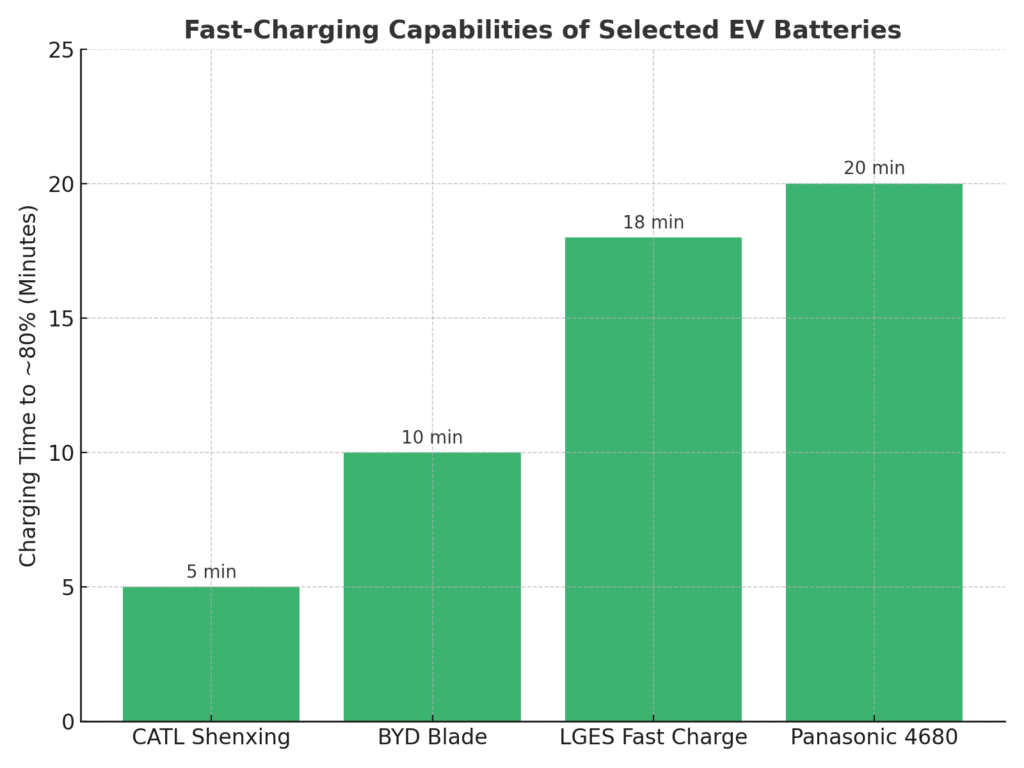

- Technological Edge: Second-generation Shenxing battery enables ~520 km range in 5 minutes of charging, exceptional cold-weather performance, and ultra-fast charging speeds.

- Strategic Positioning: Extensive OEM partnerships (Tesla, BMW, VW, etc.), vertical integration into raw materials, and early commercialization of sodium-ion batteries.

2. BYD / FinDreams

- Global Market Share: ~16–17%.

- Key Innovation: Blade Battery — ultra-safe LFP format with long cycle life and reduced thermal runaway risk.

- Deployment: Powers BYD’s own extensive EV lineup and is licensed to external automakers.

3. LG Energy Solution (LGES)

- Global Market Share: ~14%.

- Chemistries: NCM, NCMA, and ongoing solid-state R&D.

- OEM Clients: GM, Ford, Volkswagen, Stellantis.

- Strategic Moves: Multiple joint ventures with U.S. automakers; positioned as a key enabler of North America’s EV manufacturing base.

4. Panasonic Energy

- Historic Role: Longtime Tesla supplier; pioneer in cylindrical lithium-ion cells (NCA chemistry).

- Scaling Efforts: Launching large-scale 4680 cell production in Japan and the U.S., with a new $4 billion Kansas facility adding ~32 GWh/year capacity.

- Philosophy: Optimizing existing lithium-ion formats while cautiously approaching solid-state deployment.

5. Samsung SDI

- Global Share: ~5%.

- OEM Partnerships: Hyundai (cells from 2026), BMW, Stellantis.

- R&D Direction: Pursuing high-energy-density solid-state cells for early 2030s market entry.

6. EVE Energy

- Global Share: ~2.3%.

- Major Contracts: BMW Neue Klasse (Hungary plant), U.S. JV for commercial EVs.

- Technologies: LFP and NCM chemistries tailored for both consumer EVs and heavy transport.

7. Sunwoda

- OEM Reach: Geely, VW, Volvo, Li Auto.

- Production Footprint: China, Hungary, India, Morocco, Vietnam.

- Positioning: Rapidly scaling to challenge mid-tier incumbents through geographic diversification.

8. GM Ultium Cells (GM + LGES JV)

- Chemistry: Proprietary NCMA pouch cells.

- Deployment: Standardized across GM BEVs; supply agreements with Honda/Acura.

- Facilities: Multi-state U.S. footprint with massive scaling potential.

9. WeLion (Semi-Solid-State Leader)

- Innovation: 150 kWh semi-solid-state pack with ~360 Wh/kg energy density, enabling ~1,050 km range.

- Deployment: Already in NIO ET7 sedans via swappable pack architecture.

10. ProLogium (Solid-State Pioneer)

- Current Status: Pilot-scale solid-state production in Taiwan; Dunkirk gigafactory (France) under development for 2027.

- Outlook: Aiming for first solid-state EV deployment in the next 2–3 years.

Comparative Technology Metrics

Figure 2 — Energy Density of Key EV Battery Technologies:

Figure 3 — Fast-Charging Performance Across Leading EV Batteries:

Technology Trends and Market Dynamics

- Chemistry Diversification — OEMs are no longer tied to one battery chemistry; LFP, NCM, LMFP, sodium-ion, and semi-solid-state are all in active commercial use.

- Regionalization of Supply Chains — Driven by geopolitics, tariffs, and incentives like the U.S. Inflation Reduction Act.

- Charging Speed Arms Race — CATL and BYD are pushing sub-10-minute charge times as a key differentiator.

- Solid-State Transition — Still years from mass-market, but early semi-solid deployments (WeLion) are proving feasibility.

Conclusion: The Next Decade in Perspective

The EV battery industry is entering a period of intense scale-up and technological divergence. China’s CATL and BYD remain dominant, but South Korean and Japanese firms are leveraging Western partnerships to secure regional footholds. Semi-solid-state and future solid-state batteries will gradually erode lithium-ion’s dominance, but for the near term, incremental improvements to existing chemistries and massive capacity expansion will define the competitive race.

For investors, policymakers, and industry strategists, these companies are not merely suppliers — they are gatekeepers of the electric transition. The winners will be those who can scale without sacrificing innovation, navigate geopolitical supply constraints, and integrate their products into OEM ecosystems at speed.

Key Sources on EV Battery Manufacturers & Technologies

Global Market Share & Industry Scale

- SNE Research reports that in H1 2025, CATL captured 37.9% and BYD 17.8% of global EV battery installations (280.8 GWh total) (CnEVPost).

- AlphaSense notes CATL’s leading market share of 38% and projects global demand for EV batteries to exceed 1 TWh in 2025 (AlphaSense).

- Wikipedia provides a 2023 breakdown showing market shares: CATL 37%, BYD/FinDreams 16%, LG Energy Solution 14%, Panasonic 6%, Samsung SDI 4.6%, with others following (Wikipedia).

Energy Density & Semi-Solid Advances

- WeLion’s semi-solid-state battery cells achieve 360 Wh/kg energy density, deployed in NIO’s 150 kWh swappable packs (Wikipedia).

- The WeLion website confirms their semi-solid cells’ energy density of up to 350 Wh/kg, surpassing traditional lithium-ion limits (welion-energy).

Ultra-Fast Charging Breakthroughs

- EE Times and ElectricCarsReport detail CATL’s Shenxing battery, capable of delivering 520 km range in just 5 minutes of charging (EE Times).

- Financial Times covers CATL’s Shenxing battery still charging quickly in cold climates and its imminent integration into over 67 EV models, highlighting its 800 km range capability (Financial Times).

- Business Insider reaffirms this breakthrough and mentions CATL’s sodium-ion battery offering up to 500 km range, signaling broader tech diversification (Business Insider).

Further Reading & Context

- IEEE Spectrum offers a technical overview of semi-solid battery benefits and WeLion’s performance in real-world packs (IEEE Spectrum).

- The International Energy Agency (IEA) projects global EV battery demand to surpass 3 TWh by 2030, emphasizing the urgency for scalable supply chains (IEA).

- Wikipedia’s Solid-State Battery page explains the theoretical energy density advantages of solid-state over lithium-ion batteries, reaching above 350 Wh/kg (Wikipedia).

Suggested Citations & Further Reading List

| Source | Description |

|---|---|

| SNE Research | H1 2025 global EV battery market share figures (CATL, BYD) (CnEVPost) |

| AlphaSense | CATL’s market dominance and global EV battery demand forecast (AlphaSense) |

| Wikipedia (Battery Manufacturers) | 2023 production and market share overview (Wikipedia) |

| WeLion (Wikipedia & IEEE) | Semi-solid-state cell energy density and deployment in NIO EVs (Wikipedia, IEEE Spectrum) |

| WeLion official site | Energy density specs and roadmap for semi-solid batteries (welion-energy) |

| EE Times & ElectricCarsReport | CATL Shenxing battery fast-charge capability details (EE Times, Electric Cars Report) |

| Financial Times | Cold-weather performance, model deployment, and sodium-ion innovation (Financial Times) |

| Business Insider | Fast-charging range figures and Naxtra sodium-ion battery overview (Business Insider) |

| IEA Global EV Outlook 2025 | Future demand trajectory for EV battery installations (IEA) |

| Wikipedia (Solid-State Batteries) | Energy density benefits and future potential of solid-state tech (Wikipedia) |

Disclaimer – Betweenplays Media

Betweenplays Media is a content-driven platform, delivering market insights, technology coverage, and geopolitical analysis for informational and educational purposes only. The views expressed are those of the authors and guests, based on publicly available information, personal analysis, and opinion. Nothing in this publication should be interpreted as investment advice, financial recommendations, or a solicitation to buy or sell any security. Always conduct your own research or consult a qualified financial professional before making any investment decisions. Betweenplays Media assumes no liability for any loss or damages arising from the use of this information.