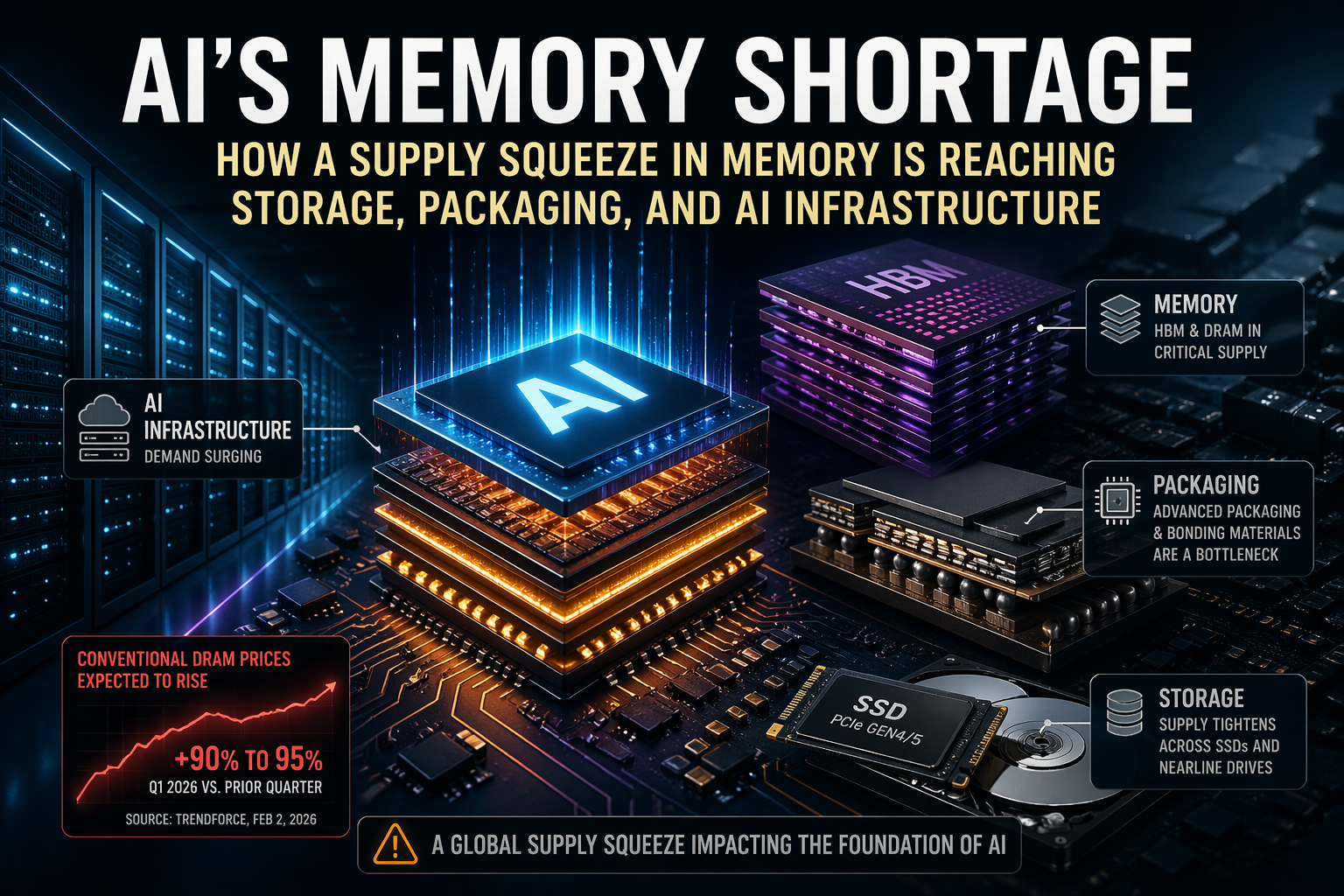

How The Supply Squeeze Extends Beyond RAM Into Storage and Advanced Packaging

MONTREAL, April 20, 2026 — The current semiconductor shortage is centered on memory rather than a broad consumer hard-drive shortfall. Samsung projected an eightfold jump in first-quarter operating profit on April 6, citing stronger AI-chip demand and higher memory prices, while TrendForce said on February 2 that conventional DRAM contract prices were expected to rise 90% to 95% in the first quarter from the previous quarter. Reuters also reported on January 29 that Samsung and SK hynix said PC and smartphone makers were facing tighter supplies as producers prioritized more profitable memory used in AI infrastructure. (Reuters)

The supply shift is concentrated in high-bandwidth memory, or HBM, the stacked memory used with AI accelerators. Reuters reported on January 14 that SK hynix was moving up the opening of a new fab in Yongin to February 2027 and starting operations at its M15X fab in Cheongju in early 2026 to respond to rising memory demand. Reuters also reported on January 28 that Samsung expected the shortage to persist through 2026 and potentially into 2027, with limited near-term supply expansion and sustained AI-related demand. (Reuters)

The current cycle differs from earlier memory shortages because the constraint is no longer limited to front-end wafer capacity. Reuters reported on March 10 that Applied Materials partnered with Micron and SK hynix on next-generation memory for AI and high-performance computing, including advanced materials, process integration, and 3D packaging. That places part of the bottleneck in the back end of semiconductor manufacturing, where stacked dies must be bonded, insulated, and packaged at high yield. (Reuters)

Material suppliers are documenting that shift. Toray said on March 14, 2024, that it had developed a hybrid-bonding insulating resin for semiconductor packaging, and on November 26, 2025, that it had developed a temporary bonding material for wafers thinned to 30 micrometers or less, including uses in next-generation HBM for AI semiconductors. TOWA said on March 21, 2025, that its “Ultra narrow gap Mold Underfill” technology was designed for the narrow gaps in next-generation HBM4 and for vertically stacked semiconductor packages. (Toray Plastics)

The storage market is being pulled into the same cycle. Reuters reported on March 20 that Solidigm expects AI’s growing demand for data to tighten supplies of storage chips over the next several years. Seagate said in its January 27 earnings-call transcript that its nearline capacity is fully allocated through calendar year 2026 and that it expects to begin taking orders for the first half of 2027 in the coming months. (Reuters)

The memory business has followed similar supply patterns before. Princeton’s Office of Technology Assessment wrote that U.S. DRAM producers cut investment during the 1974–75 recession and were then unable to meet the demand surge in 1979, allowing Japanese manufacturers to expand their position in the market. The same OTA history says the 1979 boom created a capacity shortage among both Japanese and American producers. (Princeton University)

The next major turn came in the late 1980s. The Los Angeles Times reported on March 3, 1988, that Dataquest expected a general DRAM shortage through 1988. NBER research on U.S.-Japan semiconductor trade policy describes the 1986 semiconductor agreement as one of the most controversial trade actions of the decade and says its antidumping provisions contributed to steep price increases for some semiconductors. (Los Angeles Times)

A modern version of the cycle reappeared in 2017, when Reuters reported that memory producers were entering what analysts called an “ultra-super-cycle” as tight supply met rising demand from smartphones, data storage, artificial intelligence, autonomous driving, and the Internet of Things. Reuters then reported in January 2018 that, after roughly a year and a half of rising prices, a drop in some memory prices began to raise concerns that the upcycle was breaking. In April 2023, Reuters reported that Samsung’s quarterly profit was expected to fall to its lowest level in 14 years amid a chip glut and weaker purchases from data centers and computer makers. (Reuters)

In 2026, the same sequence has returned with AI as the demand driver: a prior downturn reduced investment, demand recovered faster than new supply could be added, producers allocated output toward higher-value segments, and shortages spread into adjacent markets. For AI systems, the constraint is no longer limited to logic chips or GPUs. It now includes HBM supply, advanced packaging capacity, bonding materials, and the storage layer feeding AI infrastructure. Micron said on March 16 that it had entered high-volume production of HBM4 designed for NVIDIA Vera Rubin and of a PCIe Gen6 data-center SSD optimized for agentic AI workloads on NVIDIA BlueField-4 STX architecture. (Reuters)

Taken together, the current shortage is a memory and packaging shortage that begins with DRAM and HBM, extends into SSDs and nearline storage, and includes the materials required to assemble advanced memory at commercial scale. (Reuters)

By COO & Editor-in-Chief Sandeep Panesar