The Race for Digital Sovereignty and the End of Tech Neutrality

For thirty years, global markets operated under a comfortable economic myth: that technology was neutral.

We treated web browsers, cloud servers, office productivity suites, mobile phones, and satellite links like digital pens and paper — colorless, borderless, and politically sterile. A spreadsheet was just a spreadsheet, whether it was hosted in Silicon Valley, Frankfurt, Dublin, or Tokyo. A search engine was just a search engine. A cloud server was just a cheaper way to rent computing power. A mobile operating system was simply the glass layer between a user and the internet.

That myth is over.

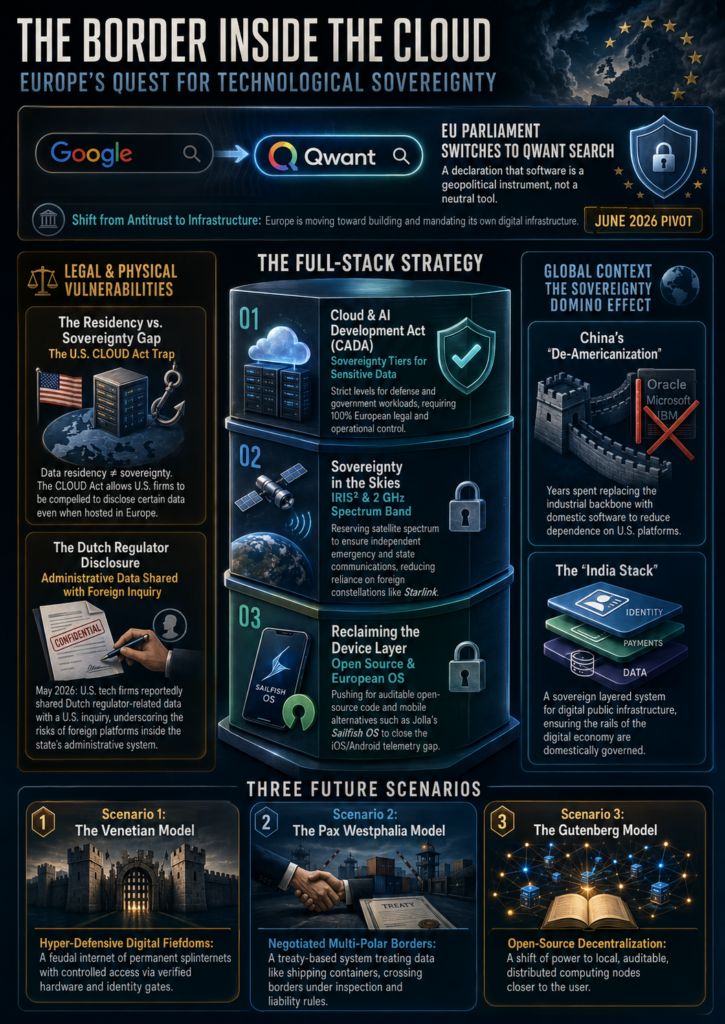

The turning point arrived quietly but definitively in June 2026. Members of the European Parliament, their staff, and administrative users opened their browsers to find that the familiar, primary-colored Google default had been replaced by Qwant, a privacy-first, French-born search engine. Changing a default browser setting sounds like a minor IT adjustment. In reality, it was an institutional declaration of intent. It marked the moment Europe moved from being a defensive referee — handing out antitrust fines and privacy rulings to Silicon Valley — toward becoming an active geopolitical player building its own digital borders.

The message is clear: software now carries a passport; and if that passport is American, European governments are increasingly asking whether their data, records, strategies, and public-sector workflows remain fully under European control.

This is not simply anti-Americanism. American technology works. Microsoft, Google, Amazon, Apple, and SpaceX built much of the modern digital world. The issue is no longer whether the tools are good. The issue is whether a sovereign government can guarantee legal immunity, operational continuity, administrative confidentiality, and strategic independence when the software, cloud, device, and satellite layers are controlled outside its jurisdiction. This is the real end of tech neutrality.

The Legal Trap: The U.S. CLOUD Act

To understand why European policymakers are now treating ordinary software procurement as a sovereignty question, you have to look past the interfaces and into the legal plumbing.

The key pressure point is the U.S. Clarifying Lawful Overseas Use of Data Act, better known as the CLOUD Act. Passed in 2018, it clarified that U.S.-based technology providers can be compelled through valid U.S. legal process to produce certain data under their control, even when that data is stored outside the United States. That does not mean every file sitting on a European server is automatically open to Washington. There are legal standards, challenge mechanisms, and conflict-of-law questions. But the strategic problem remains: data residency is not the same thing as data sovereignty.

For decades, governments assumed that if data was physically stored on European soil, it was protected primarily by European law. The CLOUD Act complicates that assumption. If a European ministry, regulator, hospital, or court system uses a U.S.-owned cloud or productivity stack, the physical geography of the server may not fully shield the data from foreign legal exposure.

That is the sovereignty fracture.

A cloud instance in Dublin, Frankfurt, or Paris may look European on a procurement form, but if the parent company remains subject to U.S. jurisdiction, the control plane may still answer to a foreign legal system. For a consumer, that may feel abstract. For a government, a regulator, a defense agency, or a court, it becomes a national-risk question.

The old model said: host the data locally. The new model says: control the company, the software, the personnel, the operating environment, the legal exposure, the encryption keys, and the emergency recovery path. Anything less is sovereignty theater.

The Smoking Gun: The Dutch Regulator Disclosure

In May 2026, Dutch media reported that Microsoft and other U.S. technology companies had shared information involving Dutch civil servants and academics with a U.S. congressional inquiry into European technology regulation. The officials reportedly included people connected to the Dutch Data Protection Authority and the Authority for Consumers and Markets — agencies involved in enforcing Europe’s digital regulatory framework.

The details matter because these were not random bureaucrats. They were part of the European machinery responsible for implementing and enforcing laws such as the Digital Services Act, the very framework designed to regulate the conduct of major technology platforms. For Europe, the lesson was brutal. Public-sector officials could use standard enterprise tools to enforce European law, while information connected to those officials could still be pulled into a foreign political process. Even if the disclosure followed a legal pathway, the political signal was unmistakable: administrative dependence creates strategic exposure.

This is why the Microsoft incident landed so hard in the sovereignty debate. It showed that the risk was not only consumer privacy, advertising profiles, or targeted marketing. It was the operational safety of regulators, civil servants, and policy actors.

The concern is no longer simply that foreign platforms can observe markets, it is that foreign platforms may sit inside the administrative nervous system of the state. For European officials, that creates an intolerable contradiction. They are asked to enforce the world’s most aggressive digital laws while relying on the tools of the companies and jurisdictions being regulated. That is not a stable architecture, but a conflict of control.

Moving Beyond Software: The Battle for the Skies

In May 2026, the European Commission proposed a new authorization regime for the 2 GHz mobile-satellite-services band after existing authorizations expire in 2027. This spectrum is strategically important because it can support mobile satellite services and direct-to-device connectivity — the ability for ordinary smartphones to communicate with satellites without requiring a specialized dish.

That matters for emergency communications, maritime connectivity, defense resilience, rural coverage, and national continuity planning. Whoever controls the satellite layer may control the backup network when terrestrial infrastructure fails. The fracture is no longer confined to cloud servers and productivity suites. It has expanded upward into the atmosphere. This is not just a software dispute. It is a contest over electromagnetic real estate.

The proposed European structure does not simply “ban” non-European providers. The reality is more precise. The Commission’s approach would reserve part of the 2 GHz band for state, security, and governmental use through European-controlled infrastructure linked to Europe’s sovereign satellite ambitions. Another portion would be oriented toward European commercial operators, while non-European operators such as Starlink or Amazon’s Project Kuiper would compete for a more limited open block.

The strategic effect is clear: Europe is no longer willing to let privately owned foreign satellite constellations become the default emergency communications layer for the continent.

This creates a split across every layer of technology.

On Earth, Europe is attempting to reduce dependence on Microsoft 365, Google Workspace, AWS, Azure, and U.S.-controlled productivity and cloud stacks by promoting alternatives such as Qwant, Nextcloud, openDesk, OVHcloud, and other European or open-source systems.

In the skies, Europe is attempting to reduce reliance on Starlink, Project Kuiper, and other non-European satellite systems by accelerating IRIS², its planned secure satellite constellation for governmental and critical communications.

The meaning is simple: sovereignty is no longer a data-center question. It is a full-stack question. Cloud. Search. Office software. Operating systems. Satellites. Spectrum. Devices. Identity. Encryption. Procurement. Legal jurisdiction. Everything is now part of the same battlefield.

The Ultimate Vulnerability: The Glass in Your Hand

Even if Europe secures its cloud infrastructure and ringfences parts of its satellite future, a glaring trillion-dollar vulnerability remains: the physical hardware through which every byte of data is accessed. Apple’s iOS and Google’s Android dominate the mobile operating system market in Europe. At the desktop and laptop layer, Microsoft Windows, Apple macOS, Google ChromeOS, and associated U.S.-controlled software environments remain deeply embedded in daily government, enterprise, and consumer use.

For European defense ministers, intelligence officers, regulators, judges, hospital administrators, and civil servants, this means the physical glass and keyboards they touch every day are governed by code written mostly outside Europe. The security risk here is foundational. Operating systems control the bare metal of the device. Even if an official uses a sovereign European cloud application, the underlying operating system can still generate telemetry, system logs, device identifiers, application behavior data, location signals, crash reports, and other metadata.

Not all telemetry is malicious. Much of it supports security, debugging, updates, and service reliability. But sovereignty is not built on good intentions. It is built on control. If the operating system, device management layer, app store, update mechanism, or telemetry pipeline sits outside sovereign jurisdiction, then the state remains dependent on a foreign platform at the most intimate layer of the stack.

The European Commission’s Open Source Strategy, published alongside the wider technological sovereignty package, recognizes this dependency problem. The strategy places open source at the center of Europe’s effort to build more resilient, auditable, and sovereign digital ecosystems. It is not only about saving money or encouraging developer communities. It is about reducing structural dependence on proprietary platforms that cannot be fully inspected, governed, or controlled by public institutions.

This is where the mobile device becomes the final border. A secure cloud is useful. A sovereign satellite network is important. But if the handset itself remains opaque, the sovereignty chain is incomplete. That explains the renewed interest in European mobile alternatives such as Jolla and Sailfish OS. Jolla’s new privacy-focused phone, shown around Mobile World Congress 2026, is not likely to overthrow Android or iOS overnight. But that is not the point. Its significance is symbolic and architectural. It shows that the sovereignty conversation has moved from servers and software licenses into the user’s pocket.

The future of digital sovereignty may not begin in a parliament or a data center. It may begin with whether a civil servant can hold a device that does not quietly answer to someone else’s cloud.

The Twin Engine: The European Technological Sovereignty Package

The Qwant shift, the cloud debate, the satellite spectrum proposal, and the open-source push are not isolated events. They are part of a wider European policy turn.

At the center of that turn is the European Technological Sovereignty Package, driven by Executive Vice-President Henna Virkkunen and framed around reducing strategic dependence on non-European technology providers. The core legislative proposal is the Cloud and AI Development Act, or CADA.

CADA is designed to strengthen Europe’s cloud and AI ecosystem, expand infrastructure capacity, support investment, and define what cloud and AI sovereignty actually mean for public-sector use. Most importantly, it introduces a sovereignty assessment framework built around assurance levels. That matters because Europe is beginning to draw a line between ordinary digital services and highly sensitive public-sector workloads.

For general public data, Europe may still allow non-European hyperscalers to compete if they meet strict conditions around residency, security, operational controls, and resilience. But for sensitive government, defense, healthcare, judicial, and critical-infrastructure workloads, the direction of travel is much more restrictive. The underlying logic is clear: the more sensitive the data, the more complete the sovereignty requirement.

At the highest levels, sovereignty cannot simply mean a European data center operated by an American parent company. It must mean European legal control, European operational control, European governance, European personnel constraints, European key custody, and European recovery capability.

That is why the phrase “sovereign cloud” is becoming dangerous. It can mean almost anything if left undefined. A U.S. hyperscaler with a European region may call itself sovereign. A joint venture may claim local control. A cloud provider may promise ringfenced operations. But Europe is now asking a harder question:

Who has the final authority when law, politics, crisis, and infrastructure collide?

If the answer is not Europe, the system is not fully sovereign.

The Cost of Sovereignty

This shift will not be frictionless. European alternatives may be less mature, less integrated, more expensive, and slower to deploy than the dominant U.S. platforms. Migration away from Microsoft, Google, Amazon, Apple, and other hyperscale ecosystems will be technically painful. Procurement will get more complicated. Compatibility will suffer. Training costs will rise. Public-sector IT departments will have to relearn systems that had become invisible through habit.

That matters because the case for digital sovereignty becomes weaker if it pretends there is no cost. There is a cost. In the short term, it may mean lower convenience, higher integration friction, and weaker user experience. The strategic trade-off is no longer convenience versus ideology.

It is convenience versus control.

For a private company, convenience may win. For a sovereign state, control eventually becomes non-negotiable.

The Trillion-Dollar Crack in the Silicon Wall

For decades, the standard Wall Street investment thesis for mega-cap technology was simple: their dominance was protected by an unbreachable moat.

Once a business, school district, hospital, ministry, or national government integrated into an American digital ecosystem, the cost and complexity of leaving made them customers for life. Microsoft owned the productivity layer. Google owned search, advertising, Android, and browser behavior. Amazon owned the scalable cloud. Apple owned premium devices. SpaceX was becoming the default name in resilient satellite connectivity.

The race for digital sovereignty is draining that moat.

If public sectors around the world begin to decouple from American technology infrastructure, the financial impact will not appear in one dramatic quarter. It will appear gradually across procurement cycles, licensing renewals, public tenders, cloud migration programs, satellite authorizations, device refreshes, and national security contracts.

That is how moats fail, not all at once. One default at a time.

The Dismantling of the Default

Microsoft, Google, and Apple face an immediate symbolic threat from the dismantling of default behavior. Google’s model is especially exposed to the psychology of defaults. Search dominance is not only a technical achievement. It is also behavioral infrastructure. The default search engine captures intent before the user makes an active choice. It shapes habits, advertising loops, query data, and profile construction.

By moving to Qwant, the European Parliament did not destroy Google’s business. But it punctured the assumption that Google is the inevitable institutional default. That matters because the default is where power hides. If public-sector defaults shift, private-sector habits can follow. If private-sector habits shift, advertising data changes. If advertising data changes, market power changes. This is why a browser setting can carry geopolitical weight.

Locked Out of the Sky, the Cloud, and the Device Stack

The most violent long-term contraction may occur across infrastructure, aerospace, and hardware. Amazon Web Services, Microsoft Azure, and Google Cloud have spent years building European data centers and local compliance programs to win public-sector trust. But if CADA and related procurement rules define high-sensitivity workloads through ownership, governance, and legal-control criteria, then physical presence alone will not be enough.

That places a ceiling on the most sensitive European public-sector cloud opportunities available to non-European hyperscalers.

At the satellite layer, the 2 GHz proposal sends a similar signal. Europe does not want its next-generation emergency connectivity, maritime communications, public safety infrastructure, and defense-adjacent satellite services to become permanently dependent on foreign commercial constellations.

At the device layer, the pressure is more nascent but equally important. If European procurement begins to prioritize device neutrality, open bootloaders, open operating systems, local device management, and auditable software stacks, Apple and Google could eventually face pressure in their most profitable enterprise channels.

This will not happen overnight. Android and iOS are entrenched. Microsoft Windows is entrenched. AWS and Azure are entrenched. Starlink is technologically powerful, but sovereignty is not a quarterly trend. It is a generational procurement doctrine. Once governments start writing sovereignty requirements into tenders, the market reorganizes around them.

The Global Domino Effect

This structural decoupling is not limited to Brussels and Paris. Europe is providing a Western blueprint for a trend that is already visible elsewhere. China has been moving through its own de-Americanization process for years. State directives have pushed critical sectors, state-owned enterprises, energy, finance, and government systems toward domestic software and hardware alternatives. The logic is not subtle. China does not want its administrative or industrial backbone dependent on Microsoft, Oracle, IBM, or other foreign-controlled platforms.

India followed a different path. Rather than only replacing foreign technology, it built a sovereign digital public infrastructure through India Stack — a layered system for identity, payments, verification, and digital services. India’s model is not isolationist in the same way as China’s, but it is deeply sovereign. It ensures that the rails of the digital economy are not entirely owned by foreign corporate platforms.

Across the Global South, the lesson is becoming obvious. No country wants its digital nervous system controlled by a foreign corporate legal team answering to a foreign capital. Cloud dependence, platform dependence, satellite dependence, mobile OS dependence, and AI infrastructure dependence are now recognized as geopolitical dependencies.

The global internet is not disappearing, but the borderless internet is being replaced by jurisdictional infrastructure.

The Geopolitical Fracture: Three Scenarios for the Digital Renaissance

This rapid decoupling reveals a profound truth: the decades-old geopolitical alliance between the United States and its Western allies is being stressed by the architecture of technology itself.

Technology is no longer merely an economic utility. It is a raw instrument of national power, comparable to energy, territory, currency, shipping lanes, semiconductors, and military communications.

The current moment bears a cautionary resemblance to earlier periods of fragmentation. When a central system weakens, regions retreat into defensible structures. The collapse of Roman authority in Europe did not immediately produce modernity. It produced localism, fortification, fragmentation, and survival logic.

But fragmentation was not the end of history. It also created the conditions for new architectures of trade, governance, finance, science, and eventually the Renaissance.

The borderless internet may be entering its own early medieval phase. The question is what comes next.

Three scenarios are now visible.

Scenario 1: The Venetian Model — Hyper-Defensive Digital Fiefdoms

In this scenario, the global internet begins to resemble 15th-century Italy: a fractured landscape of fiercely independent, commercially sophisticated, heavily defended city-states.

Instead of a single global web, the world hardens into permanent splinternets. Europe locks down its sovereign cloud tiers and moves civil servants onto audited devices. China completes its domestic substitution strategy. The United States doubles down on its corporate hyperscale stack as an instrument of national leverage.

The public web becomes increasingly polluted by AI-generated content, automated influence operations, bot-to-bot traffic, synthetic fraud, and low-trust information markets. Authentic human culture and high-value intellectual exchange retreat into closed, verified, hardware-secured networks.

The internet does not die.

It becomes feudal.

Access is controlled. Identity is verified. Hardware is trusted. Local rules dominate. The open web becomes the noisy exterior. Serious institutional life moves behind gates.

In this model, sovereignty is achieved through defense.

Scenario 2: The Pax Westphalia Model — Negotiated Multi-Polar Borders

The second scenario mirrors the post-Renaissance move toward the Peace of Westphalia: not total isolation, but a formal recognition of sovereign borders.

In this model, the major digital blocs stop pretending the internet is borderless. Instead, they negotiate rules.

Data traffic is treated more like shipping containers. It moves across borders, but under declared jurisdiction, inspection rules, treaty obligations, security guarantees, and liability structures. Cloud providers operate internationally, but only by accepting hard local-control requirements. Device makers sell into foreign markets, but with stricter obligations around telemetry, app-store control, bootloader access, procurement transparency, and data portability.

The idea of one seamless World Wide Web gives way to a treaty-based network of networks.

This is not as open as the old internet dream. But it may be more stable than the splinternet.

In this model, sovereignty is achieved through negotiation.

Scenario 3: The Gutenberg Model — Open-Source Decentralization

The third scenario is the most radical and potentially the most democratic.

It mirrors the effect of the printing press, which redistributed knowledge away from centralized authorities and toward broader public, civic, and commercial networks.

In this model, both corporate hyperscale monopolies and heavy-handed state control weaken under their own complexity. The energy demands of centralized AI, the rising costs of cloud infrastructure, the legal exposure of foreign platforms, and the public distrust of opaque systems create a new demand for local, open, auditable technology.

Power shifts from centralized server farms toward local computing nodes, open-source software, sovereign code bases, municipal infrastructure, community clouds, and transparent operating environments. Instead of renting everything from a foreign hyperscaler or relying on proprietary black-box devices, governments and communities run smaller, distributed, inspectable systems closer to where the data is created.

This does not mean the end of global computing. It means the end of blind dependence.

Open source becomes not just a developer preference, but a sovereignty mechanism.

Human attention and sovereign thought are protected not by state-built walls alone, but by the physical distribution and auditability of the technology itself.

In this model, sovereignty is achieved through decentralization.

The Long-Term Macro Bet

Whether the global landscape settles into defensive digital fiefdoms, negotiated multi-polar borders, or decentralized open-source infrastructure, one reality remains clear: long-term autonomy is now worth a short-term drop in convenience.

When the European Parliament moved its search default to Qwant, it signaled that browser behavior had become a sovereignty question.

When the European Commission moved on cloud and AI sovereignty through CADA, it signaled that data residency was no longer enough.

When Brussels proposed a new 2 GHz satellite authorization regime, it signaled that the sky itself had become part of the digital border.

When Europe placed open source at the center of its sovereignty strategy, it signaled that code transparency had become a public-interest issue.

The comfortable myth of tech neutrality is gone.

Software has a passport.

Clouds have jurisdictions.

Satellites have strategic owners.

Devices have loyalties.

The global market will no longer be won only by software that claims to change the world. It will be won by infrastructure that respects the legal, physical, and political realities of the borders it operates within.

For investors, this is not a recommendation to buy or sell any specific security. It is a structural warning. The market has spent decades pricing American technology platforms as if their global reach was permanent. Digital sovereignty challenges that assumption.

The moat is still there.

But the water level is falling.

Verified Reference List

European Commission. “Proposal for the Cloud and AI Development Act (CADA).” Published June 3, 2026.

https://digital-strategy.ec.europa.eu/en/library/proposal-cloud-and-ai-development-act-cada

European Commission. “Cloud and AI Development Act.”

https://digital-strategy.ec.europa.eu/en/policies/cloud-and-ai-development-act

European Commission. “Communication on European Tech Sovereignty, accompanied by an EU Open Source Strategy.” Published June 3, 2026.

https://digital-strategy.ec.europa.eu/en/library/communication-european-tech-sovereignty-accompanied-eu-open-source-strategy

European Commission. “The EU Open Source Strategy.”

https://digital-strategy.ec.europa.eu/en/policies/open-source-strategy

Reuters. “EU Parliament to switch to French search engine from Google in tech sovereignty push.” Published June 3, 2026.

https://www.reuters.com/business/eu-parliament-switch-french-search-engine-google-tech-sovereignty-push-2026-06-03/

Reuters. “EU targets Big Tech dependence with ‘made-in-Europe’ drive.” Published June 3, 2026.

https://www.reuters.com/business/eu-targets-big-tech-dependence-with-made-in-europe-drive-2026-06-03/

Reuters. “EU cloud rules to curb Big Tech’s access to strategic tenders, draft document shows.” Published June 1, 2026.

https://www.reuters.com/business/retail-consumer/eu-cloud-rules-curb-amazon-google-access-strategic-tenders-draft-document-shows-2026-06-01/

Reuters. “European companies to get bulk of mobile satellite spectrum in EU tech push.” Published May 27, 2026.

https://www.reuters.com/business/media-telecom/european-operators-get-bulk-mobile-satellite-spectrum-rest-non-eu-rivals-eu-says-2026-05-27/

European Commission. “Commission proposes new authorisation for mobile satellite services.” Published May 2026.

https://ec.europa.eu/commission/presscorner/detail/en/ip_26_1170

DutchNews.nl. “US tech firms share Dutch regulator officials’ names with senate.” Published May 22, 2026.

https://www.dutchnews.nl/2026/05/us-tech-firms-share-dutch-regulator-officials-names-with-senate/

NL Times. “Microsoft accused of leaking Dutch civil servants’ names to U.S. government.” Published May 22, 2026.

https://nltimes.nl/2026/05/22/microsoft-accused-leaking-dutch-civil-servants-names-us-government

Free Software Foundation Europe. “EU Tech Sovereignty: A milestone for Public Code? Now implementation is key.” Published June 3, 2026.

https://fsfe.org/news/2026/news-20260603-01.en.html

Microsoft. “The CLOUD Act: What It Is and What It Is Not.”

https://cdn-dynmedia-1.microsoft.com/is/content/microsoftcorp/microsoft/msc/documents/presentations/CSR/CLOUD-Act-What-it-is-and-is-not.pdf

Jolla. Corporate information and product background.

https://jolla.com/

Wired. “The ‘European’ Jolla Phone Is an Anti-Big-Tech Smartphone.” Published March 2026.

https://www.wired.com/story/jolla-phone-2026/

StatCounter. “Mobile Operating System Market Share Europe.”

https://gs.statcounter.com/os-market-share/mobile/europe/